How to Legally Minimise Property Taxes in Australia (Without Hurting Your Investment Returns)

Smart investors know property taxes can make or break returns. Learn how to reduce your tax burden legally through the right ownership structures, capital gains strategies, and deductions, all while maximising long-term wealth.

If you’re a property investor in Australia, what you don’t know could cost you tens of thousands of dollars through tax time. Whether you’re buying, selling, or simply managing your portfolio, understanding how property tax works can help you keep more of your money in your pocket.

Many Australians overlook the importance of structure. The way you buy, hold, or sell your property can completely change your tax outcome. Knowing which deductions you can claim and when to act can make all the difference.

Understanding Property Taxes in Australia

As a property investor, you’ll deal mainly with two types of taxes: capital gains tax (CGT) and income tax. Let’s go through both.

Capital gains tax is applied when you sell an investment and make a profit.

For example, if you bought a property for $600,000 and sold it for $1 million, your capital gain is $400,000.

Take note: This is before factoring in additional costs like stamp duty, buyers agent fees, and selling commissions.

These costs form part of your “cost base” and reduce the taxable gain. So, if your total costs were $60,000, your actual taxable profit becomes $440,000 instead of $500,000.

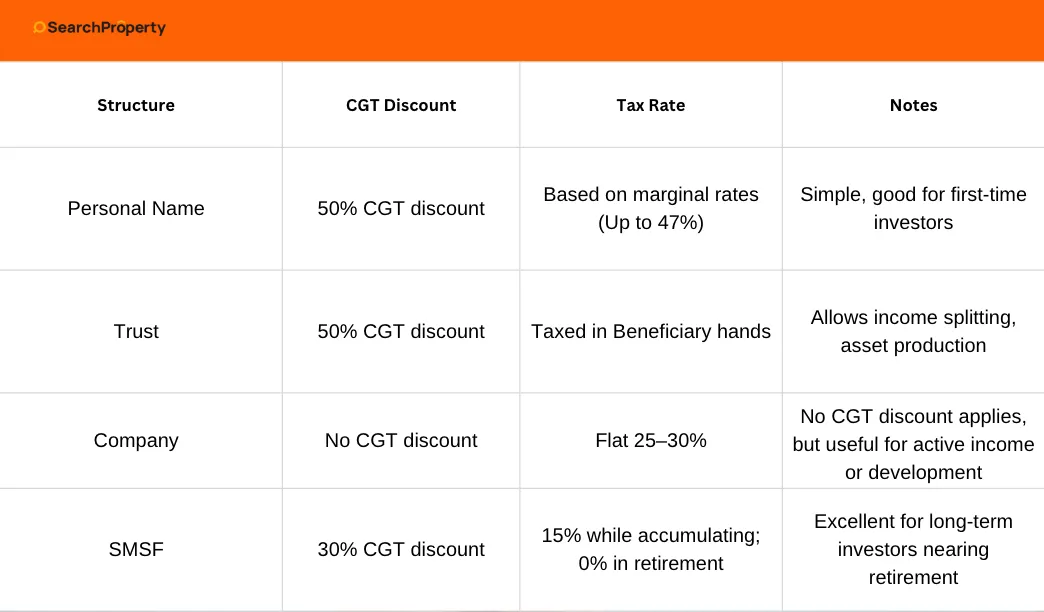

If the property was held in your personal name and you owned it for more than 12 months, you’ll receive a 50% capital gains discount. That means you’ll only pay tax on half the profit, in this case, $220,000. The tax you pay will then depend on your marginal tax rate.

Holding assets long term can make a huge difference to how much tax you owe, which is why many wealthy investors choose to buy and hold for at least 12 months before selling.

How CGT Works Across Different Structures

The way you own your property, whether it’s in your personal name, a trust, a company, or a self-managed super fund (SMSF), will also affect how much tax you pay.

If you hold property in your SMSF, you’ll pay only 15% tax while the fund is accumulating, and 0% tax once you’re in retirement. While there are more rules and fewer lenders willing to finance SMSF loans, many Australians still use this structure to build long-term wealth through real estate.

How Income Tax Applies to Property

Even if you’re not selling any properties, you can still benefit from smart tax management through income tax deductions. This is where the concept of positive and negative gearing comes in.

Positive gearing means your property earns more income than expenses. This is great for cash flow, but you’ll pay tax on that income.

Negative gearing means your expenses exceed your income, and that shortfall can reduce your taxable income.

For example, if you earn $100,000 a year and your investment property runs at a $10,000 loss, the Australian Taxation Office (ATO) may tax you as if you only earned $90,000.

This is why some accountants suggest buying property. It can legally reduce how much tax you pay each year. But there’s a catch. Some accountants focus solely on deductions and refer clients to off-the-plan or house-and-land package deals, which might not actually grow in value.

Tax savings are great, but your main goal as an investor should always be long-term capital growth.

What You Can Claim as a Property Investor

You can claim many ongoing property-related expenses, including:

Depreciation is one of the most powerful tools you can use to reduce taxable income. A quantity surveyor can assess how much your property has depreciated and prepare a report that lets you claim that amount each year.

For example, if your building cost $400,000 to construct and has a 40-year effective life, you could depreciate $10,000 per year. Even if your property earns $5,000 in positive cash flow, this depreciation could make your property appear negatively geared on paper, reducing how much tax you pay.

This is one reason why many investors prefer buying newer properties: they often provide both strong growth potential and higher depreciation benefits.

Building Wealth the Smart Way

You shouldn’t buy property just to reduce taxes. The real goal is to build wealth through smart property selection, cash flow management, and long-term strategy.

Your focus should shift depending on where you are in your investment journey:

During the acquisition phase, you use leverage and debt to build your portfolio.

Once your portfolio matures, you can move into debt reduction and cash flow optimisation.

That’s how investors create sustainable, long-term wealth, not just short-term tax benefits.

Take Action and Get Expert Guidance

Australia’s tax system is complex, but with the right team, you can minimise your taxes while growing your wealth.

If you’re ready to take the next step, book a FREE discovery call with our team at Search Property. We’ll help you understand your next move, structure your portfolio correctly, and choose properties that perform for both growth and tax efficiency.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)