What the 2026 Negative Gearing Changes Mean for Australian Property Investors.

Negative gearing has long been a hot topic in Australia's property market. Politicians, economists, and investors continue to debate whether it should stay or go. The question is no longer hypothetical. The 2026 federal budget changed the rules and the effects are already playing out in real time.

For you as an investor, the impact goes beyond tax benefits. It affects property prices, the rental market, and the way you build long-term wealth. Here is a breakdown of what has changed, and what it means for your strategy.

Negative gearing happens when the rental income you earn from a property is less than your holding costs including mortgage interest, rates, maintenance, and insurance. That shortfall is a loss you could previously offset against your taxable income in the year it occurred.

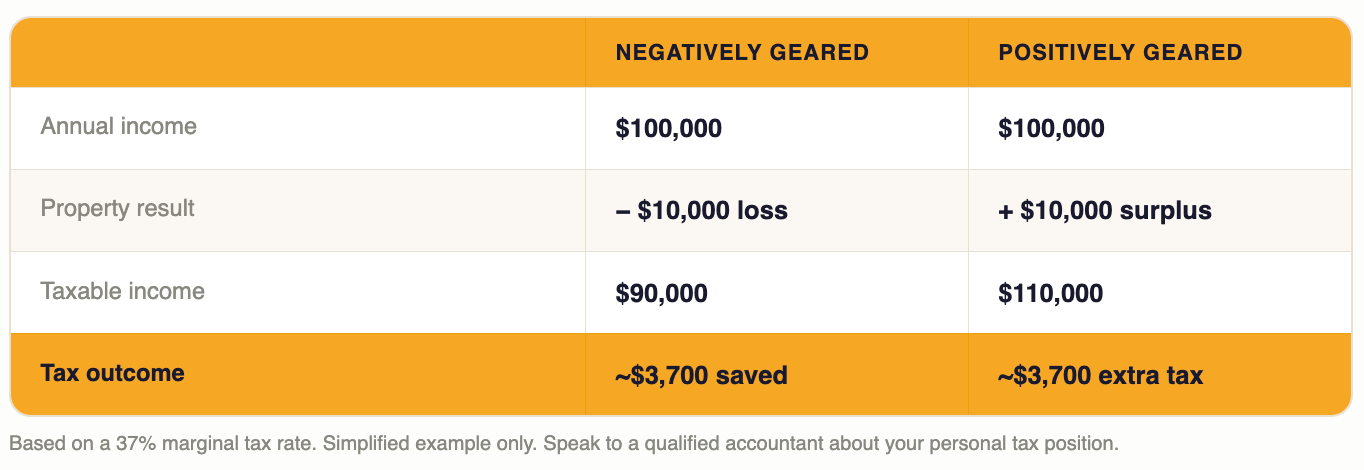

For example:

You earn $100,000 per year

Your investment property makes a $10,000 loss

With negative gearing, you are taxed on $90,000 instead of $100,000

This tax deduction made holding a property easier in the early years, particularly when rental income did not yet cover costs.

Positive gearing is the opposite. When rental income exceeds expenses, the surplus is added to your taxable income.

What Has Changed in 2026?

The 2026 federal budget did not abolish negative gearing entirely. It changed who can access it and when.

For established residential properties purchased after 7:30pm on 12 May 2026, losses can no longer be offset against wages or salary income in the year they occur. Instead they carry forward and offset future property income only.

Properties exchanged before that date are fully grandfathered. Negative gearing continues to apply to those assets for as long as you hold them.

New builds, house and land packages, and off-the-plan apartments retain full negative gearing under the new rules. The 50% CGT discount is also being replaced from 1 July 2027 with cost base indexation and a 30% minimum tax rate on real capital gains.

What Happens When Investor Incentives Are Reduced?

History gives us the clearest answer. When negative gearing was removed in Australia in 1985, rents surged in Sydney and Perth where rental supply shortages were most acute. The policy was reversed within two years because it did not deliver the intended affordability benefits and hurt the people it was designed to help.

The 2026 changes are producing similar early signals. According to Cotality's Rental Review Q2 2026, national rents have accelerated to 5.9% annually with the median national weekly rent now sitting at $705. Every capital city vacancy rate is below 2.0%. Adelaide sits at 1.0%.

When investors exit or reduce activity in the rental market, several things happen simultaneously:

Short-term pain for some investors. Those who purchased primarily for tax benefits rather than capital growth may struggle to hold on. Without the immediate offset, properties running at a significant cash flow deficit become harder to justify. This could trigger a sell-off of poorly performing or over-leveraged assets.

Downward pressure on some property prices. Segments of the market heavily reliant on investor demand may experience softness. Quality properties in undersupplied markets with genuine rental demand are significantly more resilient because owner-occupier demand remains strong regardless of investor tax settings.

Rental market pressure accelerates. Fewer investors buying means fewer rental properties added to an already critically undersupplied market. Developers are also pulling back as investor demand softens and margins thin. Fewer new starts today means fewer completions in 12 to 24 months, adding further pressure to a market already running a significant housing deficit.

A sharper divide between strategies. Investors who bought for tax deductions rather than growth are most exposed. Investors focused on capital growth and positive cash flow in supply-constrained markets are significantly better positioned regardless of what tax settings apply.

What About the CGT Changes?

From 1 July 2027 the existing 50% CGT discount is replaced with cost base indexation and a 30% minimum tax rate on real capital gains. A transitional rule applies: gains accrued before 1 July 2027 are still taxed under the existing 50% discount.

The change affects the tax paid at the point of sale but does not change the fundamental case for owning appreciating assets in supply-constrained markets over the long term.

For a detailed breakdown and CGT calculator, check out this blog.

Why the Right Strategy Matters More Than Ever

If negative gearing is no longer an immediate offset for new established property purchases, your success as an investor depends less on tax benefits and more on the quality of your asset selection and strategy.

Here is what that means in practice:

Buy for growth, not tax deductions. A property that grows in value and generates rising rental income performs regardless of tax settings. The investors most exposed to the budget changes are those who bought poor quality assets in weak growth markets specifically because of the tax offset.

Target cash flow. Properties that transition to positive cash flow within a reasonable timeframe are less dependent on any single tax concession remaining in place. Selecting assets with proper rental demand and improving yields reduces your reliance on carried-forward losses.

Think long term. Market cycles, interest rates, and policies will always change. The long-term fundamentals of supply and demand in supply-constrained markets do not. Australia is still building 196,000 homes per year against demand for more than 250,000 according to the Housing Industry

Get expert advice. Buying the wrong property in the wrong location is significantly more damaging than losing a tax benefit. A poorly selected asset with no growth and no cash flow has no saving grace regardless of tax settings.

Ready to Build a Portfolio That Performs Regardless of Tax Settings?

At Search Property, we help Australians cut through the noise and build data-driven investment strategies aligned with long-term wealth goals. Our buyers agents have helped thousands of clients build wealth through property because we focus on fundamentals, not headlines.

Book an investment assessment call with Search Property. We'll discuss your goals and position, and help you build a clear plan to move forward with confidence.

Frequently Asked Questions

Has negative gearing been abolished in Australia?

No. Negative gearing has not been abolished. The 2026 federal budget changed who can access it and when. Properties exchanged before 7:30pm on 12 May 2026 are fully grandfathered. For established residential properties purchased after that date, losses carry forward against future property income rather than offsetting wages immediately. New builds and off-the-plan apartments retain full negative gearing.

What is the difference between negative gearing and positive gearing?

Negative gearing is when your property's holding costs exceed the rental income it generates. The shortfall is a loss. Positive gearing is when rental income exceeds holding costs and the surplus is added to your taxable income. Most properties start negatively geared and transition to positive cash flow as rents rise over time.

Does negative gearing still apply to new builds?

Yes. New builds, house and land packages, and off-the-plan apartments retain full negative gearing under the 2026 rules. Losses on these properties can still be offset against wages and salary income in the year they occur.

What happens to my carried-forward losses when the property turns positive?

When your property eventually generates positive cash flow, the accumulated carried-forward losses offset that income. You effectively bank the tax saving for future use rather than losing it entirely. The deduction is simply delayed, not eliminated.

Should I still invest in property given the negative gearing changes?

Yes. The fundamental case for owning appreciating assets in supply-constrained Australian markets has not changed. The investors least affected by the budget changes are those who bought quality assets for capital growth and cash flow rather than relying on negative gearing to justify the purchase. Tax settings change but the underlying supply and demand dynamics that drive long-term property values do not.

What is the best strategy for investors under the new rules?

Focus on assets with capital growth potential and improving yields in supply-constrained markets. Prioritise properties that will transition to positive cash flow within a reasonable timeframe. Avoid assets where the entire investment case depends on an immediate tax offset rather than the quality of the underlying asset.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.