Consumer Confidence Is at a 53-Year Low. What This Means for Investors.

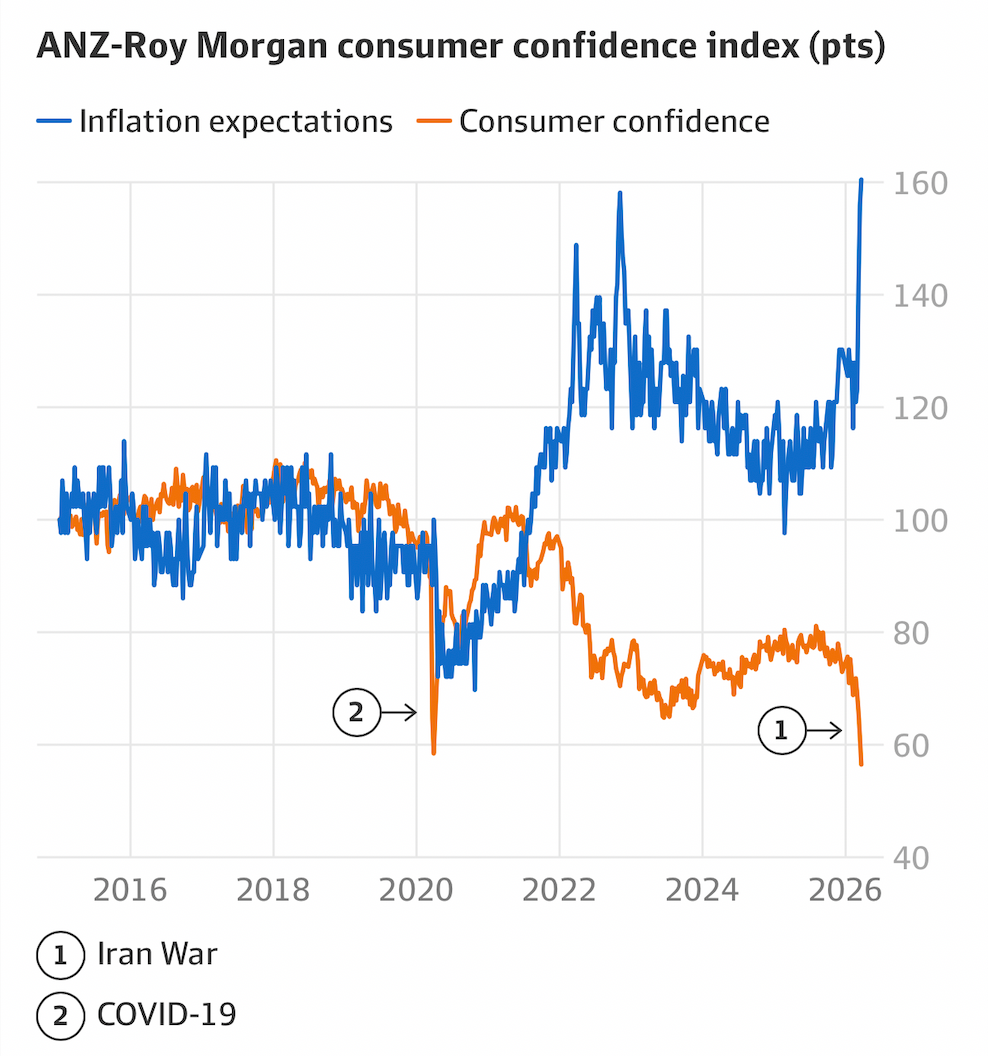

Australian consumer confidence has just hit its lowest level since 1973. In over five decades of recorded data, Australians have never felt less certain about their financial future than they do right now.

For most people, that headline is a reason to pause, wait, and see what happens next. For property investors who understand how markets actually work, it tells a very different story.

The ANZ-Roy Morgan Consumer Confidence Index has fallen to its lowest reading since records began in 1973. The decline is being driven by a combination of factors:

Future financial conditions falling by 9 points to levels below those seen during the COVID lockdowns

That last point is significant. Australians currently feel worse about their financial future than they did when the country was in lockdown, borders were closed, and nobody knew how long the pandemic would last.

The time to buy a major household item sub-index is also at its lowest point since the announcement of pandemic lockdowns in March 2020. Confidence in both present and future financial situations has declined sharply.

This is the environment investors are navigating right now.

Why Low Consumer Confidence Matters More Than Most People Realise

Consumer confidence is essentially a fear and greed index for the broader economy. When it's high, people spend freely, borrow confidently, and compete aggressively for assets. When it's low, people pull back, wait for certainty, and avoid large financial decisions.

When the economy is growing strongly, inflation rises, rates go up, and borrowing becomes more expensive. Asset prices can actually soften during periods of strong economic confidence.

When the economy weakens and rates get cut, borrowing becomes cheaper, credit flows more freely, and asset prices respond by moving higher. The lockdown period is the clearest recent example of this playing out exactly as described. Consumer confidence collapsed in early 2020. The property market subsequently delivered one of its strongest runs in Australian history.

The investors who recognised that opportunity in February and March of 2020 and acted on it have seen their portfolios grow substantially over the following years. The investors who waited for certainty are still waiting.

The K-Shaped Economy Is Accelerating

What's playing out in 2026 is an acceleration of the K-shaped economy. The divide between Australians who own assets and those who don't is widening at a pace that's becoming increasingly difficult to close.

Here's why low consumer confidence and rising rates don't necessarily mean falling property prices:

Rate hikes reduce borrowing capacity for buyers, which reduces transaction volumes

Fewer transactions means less available stock on the market

Constrained supply with any level of ongoing demand holds prices up

Rate hikes simultaneously push more people into renting, driving rental demand higher

Rising rents improve cash flow for existing investors over time

When rates eventually fall, borrowing capacity returns and demand surges

Rents rarely come down once they've gone up. Investors who hold through rate rises typically come out the other side with improved cash flow and assets that have held or grown in value. The margin between rental income and holding costs widens in their favour over time.

The people who struggle most when rates rise are not investors with buffers and strategy. They are renters with no assets, whose cost of living increases while their wealth position stays flat.

Three Types of Investors Right Now

In any uncertain market, investors tend to fall into one of three groups:

Those who can buy and will buy

These are the contrarians. They've done the work, they have buffers in place, and they understand that uncertainty creates opportunity precisely because most people step back from it. They're buying now, not because they're certain about what happens next, but because they know the fundamentals support ownership over the long term and they've structured their position to weather the volatility.

Those who can buy but are waiting

This is the largest group. They're waiting for certainty, for a clear signal that the market has bottomed, that rates have peaked, that the global situation has stabilised. On a $700,000 property, waiting while the market moves 5 to 10% higher costs between $35,000 and $70,000. That's the price of certainty. It's worth being honest with yourself about whether you're comfortable paying it.

Those who simply cannot buy

This group is growing. Rising rents, higher petrol prices, and cost of living pressures are pushing more Australians further from property ownership. This is not a market failure. It's the K-shaped economy compounding in real time. The longer this group waits, the harder the entry point becomes.

What History Tells Us About Buying When Confidence Is Low

Looking back across the last decade, the pattern is consistent.

Between 2016 and 2019, consumer confidence was relatively high. Property prices in many markets softened or went sideways. The investors who bought during that period of apparent stability didn't see the explosive growth they might have expected.

Then came 2020. Confidence collapsed. The outlook was genuinely uncertain. The following years produced some of the strongest property price growth Australia has ever recorded.

The relationship between confidence and price performance is frequently inverse. When everyone is optimistic, competition is fierce and prices reflect that optimism. When fear is dominant, competition thins out, motivated sellers appear, and patient investors with clear strategies find the best opportunities.

2026 is not 2020. The specific triggers are different. The dynamic, however, of low confidence, uncertain headlines, and investors pulling back, is creating a similar environment for those willing to look past the noise.

What Actually Drives Property Prices

The fundamental driver of Australian property prices is not consumer confidence. It is not interest rates. It is supply and demand.

Australia is not building enough homes to house its growing population. Developer activity slows when market conditions become uncertain. Construction costs remain elevated. Building approvals are not keeping pace with demand. Immigration continues to add pressure to an already constrained rental and purchase market.

A government that continues to prioritise immigration without meaningfully addressing housing supply is structurally ensuring that demand for property outpaces the available stock. This is not a short-term dynamic. It is a decade-long trend with no immediate resolution in sight.

For investors with a 10 to 20-year time horizon, short-term volatility driven by rate cycles and consumer sentiment is noise. The structural undersupply is the signal.

The Bottom Line

Consumer confidence at a 53-year low is uncomfortable. It is also, historically, one of the clearest indicators that patient investors with strong fundamentals and proper buffers are looking at an opportunity rather than a threat.

The investors who win over the next decade will be the ones who stuck to their strategy, maintained their emergency funds, and continued buying quality assets in supply-constrained markets while others waited for a certainty that never quite arrives.

The headlines change. The fundamentals don't.

Ready to Build a Strategy That Works in Any Market Condition?

At Search Property, we help Australians cut through the noise and build data-driven investment strategies aligned with long-term wealth goals. Our buyers agents have helped thousands of clients build wealth through property because we focus on fundamentals, not headlines.

Book a FREE investment assessment call with Search Property. We'll discuss your goals and position, and help you build a clear plan to move forward with confidence.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)

.png)

.png)

.png)

.png)

.png)