Australian Property Investment Cash Flow: The Complete Guide

Most property investors focus on the purchase. The investors who build serious wealth focus on what happens after the purchase, specifically how the numbers stack up on a weekly, monthly, and annual basis, and how cash flow changes across different stages of a growing portfolio.

Here is everything you need to understand about cash flow in Australian property investment.

Australian property investment cash flow is the net difference between your total rental income and total holding costs including mortgage repayments, property management fees, insurance, council rates, and maintenance. A positively geared property generates more income than it costs to hold. A negatively geared property costs more than it earns. Understanding this distinction is the starting point for every serious Australian property investor.

What Is Cash Flow in Property Investment?

Cash flow in property investment is simple in concept. It is your total rental income minus your total holding costs.

Total rental income: the weekly or monthly rent paid by your tenant, annualised.

Total holding costs include:

Mortgage repayments (interest and principal or interest only)

Property management fees (typically 7 to 10% of rent)

Council rates

Water rates

Landlord insurance

Maintenance and repairs

Strata fees if applicable

Vacancy allowance

The difference between income and costs is your cash flow position. Positive cash flow means the property puts money in your pocket. Negative means you are contributing money each week to hold it.

Positive, Negative, and Neutral Gearing Explained

Positively geared Rental income exceeds all holding costs. The property generates a pre-tax profit each week. That profit is counted as taxable income but provides ongoing passive income and improves your serviceability for future borrowing.

Negatively geared Holding costs exceed rental income. The property runs at a weekly loss. Under current rules, properties exchanged before 7:30pm on 12 May 2026 can offset those losses against other income such as wages, reducing taxable income. Properties purchased after that date as established dwellings carry losses forward against future property income only.

Neutrally geared Rental income exactly covers holding costs. No profit, no out-of-pocket contribution. Common in markets where yields have compressed as values have risen faster than rents.

A Worked Cash Flow Example

Here is a straightforward example using real dollar figures.

Property: $600,000 purchase price Loan: $540,000 (10% deposit, interest only at 6.5%) Weekly rent: $550

Annual income: $550 x 52 = $28,600

Annual holding costs:

Interest repayments: $35,100

Property management (8%): $2,288

Council rates: $1,800

Insurance: $1,500

Maintenance allowance: $1,200

Vacancy allowance (2 weeks): $1,100

Total annual costs: $43,000

Annual cash flow position: -$14,400 (approximately $277 per week out of pocket)

At a marginal tax rate of 37%, the carried-forward loss on an established property purchased post May 2026 reduces future property income by $14,400, saving approximately $5,300 in tax when offset against future property gains.

This is a negatively geared property. It costs money to hold in the short term with the expectation that capital growth and rising rents will improve the position over time.

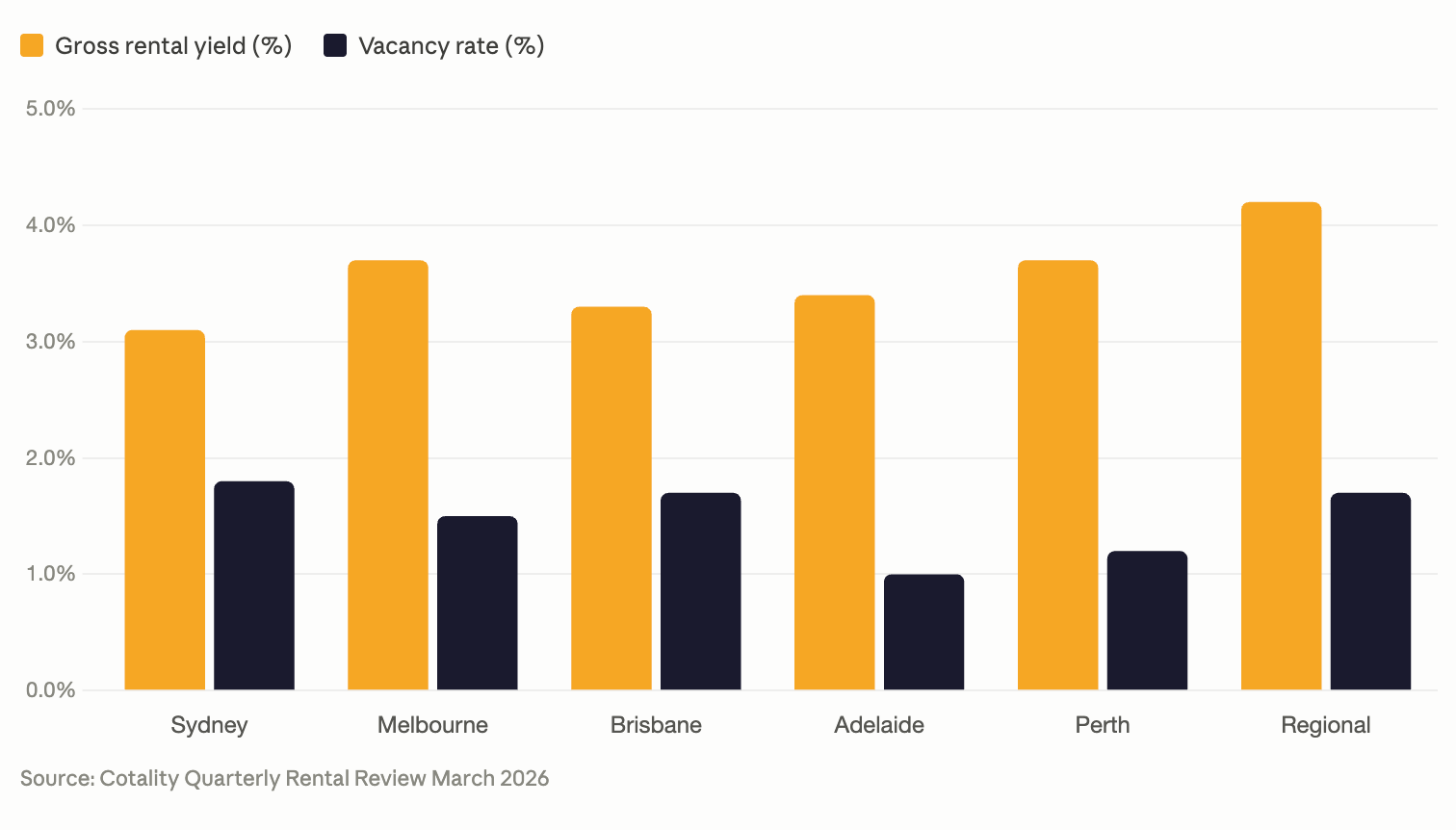

How Cash Flow Differs Across Australian Cities

Cash flow varies significantly depending on where you buy. Entry price and yield do not always move in proportion.

Sydney: gross rental yield sits at 3.1%, the lowest of all capital cities. High entry prices mean most properties run at a significant weekly cash flow deficit at current rates.

Melbourne: gross yield sits at 3.7% with vacancy at 1.5%. More accessible entry prices than Sydney produce a more manageable cash flow position, though most properties remain negatively geared at current rates.

Brisbane and Adelaide: Brisbane sits at a 3.3% gross yield with a vacancy rate of 1.7%. Adelaide offers a 3.4% gross yield with the tightest vacancy of all capitals at 1.0%. Both markets offer more accessible entry prices relative to income, producing a better cash flow position than Sydney or Melbourne.

Perth: gross yield sits at 3.7%, down from 4.3% a year ago as property values have grown faster than rents. Vacancy remains extremely tight at 1.2%.

Regional markets: combined regional gross yield sits at 4.2%, outpacing the combined capitals at 3.4%. Cash flow positive properties are most commonly found in regional Queensland, Western Australia, and South Australia where yields can reach significantly above the national average. Higher yields can come with higher vacancy risk, making thorough research on rental demand essential before buying.

Rental Yield vs Capital Growth: What Is the Difference?

Rental yield and capital growth are not the same thing and optimising for one often comes at the cost of the other.

Rental yield is the annual rental income expressed as a percentage of the property's value. A $500,000 property generating $25,000 in annual rent has a 5% gross yield.

Capital growth is the increase in the property's value over time. A $500,000 property worth $750,000 after 10 years has delivered 50% total capital growth.

The comparison between the two becomes stark over time. Consider two properties both purchased at $450,000:

Property A rents for $480 per week and grows at 7% annually. Annual capital growth: $31,500.

Property B rents for $700 per week and grows at 3% annually. Annual capital growth: $13,500.

Property B generates $220 more per week in rent. Property A generates $18,000 more in annual capital growth. Over a 10 to 20-year hold period, that gap compounds into a materially different wealth outcome.

Rental income is taxed as ordinary income each year. Capital growth is not taxed until you sell and only at a reduced rate if held longer than 12 months. That tax deferral allows wealth to compound more efficiently through capital growth than through income alone.

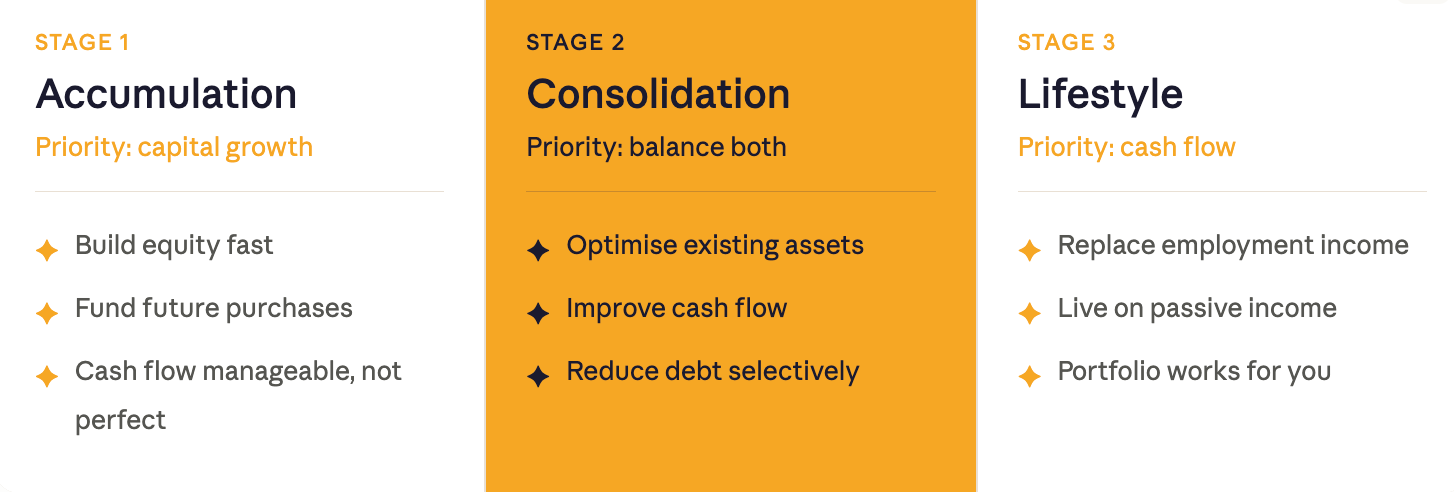

The Three Stages of Building Wealth Through Property

When to prioritise capital growth versus cash flow depends entirely on where you are in your investment journey.

Stage One: Accumulation In the early stages, capital growth is the priority. Equity from appreciating assets is the mechanism that funds future purchases without requiring new deposits from savings.

A $500,000 property growing at 7% annually is worth approximately $1.3 million after 15 years. A high-yield property in a stagnant market growing to only $900,000 over the same period represents a $400,000 wealth gap. Cash flow does not need to be strongly positive during accumulation, but it needs to be manageable enough to hold through rate movements and vacancy periods.

Stage Two: Consolidation As the portfolio grows, cash flow management becomes more important. Investors may sell high-growth assets and redeploy into stronger-yielding properties, or improve cash flow on existing assets through renovations or dual income configurations. The focus shifts from acquiring more to optimising what you have.

Stage Three: Lifestyle In the final phase, cash flow becomes the priority. The portfolio should be generating enough passive income to cover living expenses without employment income.

Capital growth builds the asset base. Cash flow funds the lifestyle. The transition between the two needs to be planned, not reactive.

You retire on cash flow, not on capital growth.

Strategies to Improve Cash Flow on Existing Properties

If a property is running a higher cash flow deficit than is comfortable, there are several approaches worth considering:

Review rent against current market rates. Many investors hold rents below market for existing tenants longer than necessary. A good property manager will benchmark rents proactively at every lease renewal.

Get a depreciation schedule. A tax depreciation schedule prepared by a quantity surveyor identifies non-cash deductions on the property's structure and fixtures, reducing taxable income without any additional cash outlay.

Add a dual income configuration. Adding a granny flat or converting to dual occupancy where zoning allows creates a second rental income stream on the same title, potentially moving a negatively geared property to a neutral or positive cash flow position.

Refinance to a more competitive rate. Reviewing your interest rate regularly is one of the simplest ways to reduce your largest single holding cost. A specialist mortgage broker can identify whether refinancing improves your cash flow position without compromising future borrowing capacity.

How the 2026 Budget Changed the Cash Flow Calculation

The 2026 federal budget introduced changes that affect how investors think about cash flow for new established property purchases.

Negative gearing on established residential properties purchased after 12 May 2026 no longer offsets wages or salary income in the year the loss occurs. Losses carry forward and offset future property income only.

For investors buying established properties, the immediate tax benefit of negative gearing is delayed rather than eliminated. This changes the short-term cash flow calculation but does not change the long-term capital growth case for well-selected assets in supply-constrained markets.

Cash flow is what keeps you in the game. Capital growth is what builds your wealth. The investors who build serious property portfolios understand both, use both, and sequence their strategy to prioritise growth early and transition toward income as the portfolio matures.

Getting the balance right at each stage of your investment journey is the difference between a portfolio that compounds quietly into genuine financial freedom and one that stalls under the weight of holding costs it was never structured to sustain.

Ready to Build a Portfolio With the Right Cash Flow Strategy?

At Search Property, we help Australians cut through the noise and build data-driven investment strategies aligned with long-term wealth goals. Our buyers agents have helped thousands of clients build wealth through property because we focus on fundamentals, not headlines.

Book a FREE Investment Assessment Call with Search Property. We'll discuss your goals and position, and help you build a clear plan to move forward with confidence.

Frequently Asked Questions

What is a good cash flow for an investment property in Australia?

It depends on your stage of investing. In the accumulation phase, a manageable negative cash flow is acceptable as long as you can hold through rate movements and vacancy periods. As rents rise and the portfolio matures, the goal shifts toward neutral and eventually positive cash flow.

How do I calculate my investment property cash flow?

Take your annual rental income and subtract all holding costs including mortgage interest, property management fees, council rates, insurance, maintenance, and a vacancy allowance. Positive means income exceeds costs. Negative means you are contributing money each week to hold it.

What is the difference between gross yield and net yield?

Gross yield is annual rental income as a percentage of the property's value before costs. Net yield deducts all holding costs including management fees, rates, and insurance. Net yield is the more meaningful figure for assessing actual cash flow and typically sits 1 to 1.5 percentage points below gross yield.

When does a negatively geared property turn positive?

As rents rise and loan balances reduce over time, the cash flow position improves. Based on conservative assumptions of 3% annual rental growth at a 6.5% interest rate, most properties trend toward neutral or positive within 10 to 15 years. Stronger rental growth or falling rates shorten that timeline.

Is positive cash flow or capital growth more important?

Both matter at different stages. Capital growth is the priority in accumulation because equity funds future purchases. Cash flow becomes the priority in the lifestyle phase because it funds living expenses without employment income. The most effective portfolios sequence growth first and transition toward income as the portfolio matures.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)