Purchasing an Investment Property Through Your SMSF

Most Australians know their superannuation is growing in the background, but very few realise it can be used to purchase investment properties. It is one of the most searched and least understood strategies in Australian property investing.

Can you use your super to buy an investment property? The short answer is yes, but only through a specific structure called a Self-Managed Super Fund. Here is a clear, straightforward breakdown of how it works, what the rules are, and whether it is worth exploring as part of your broader property investment strategy.

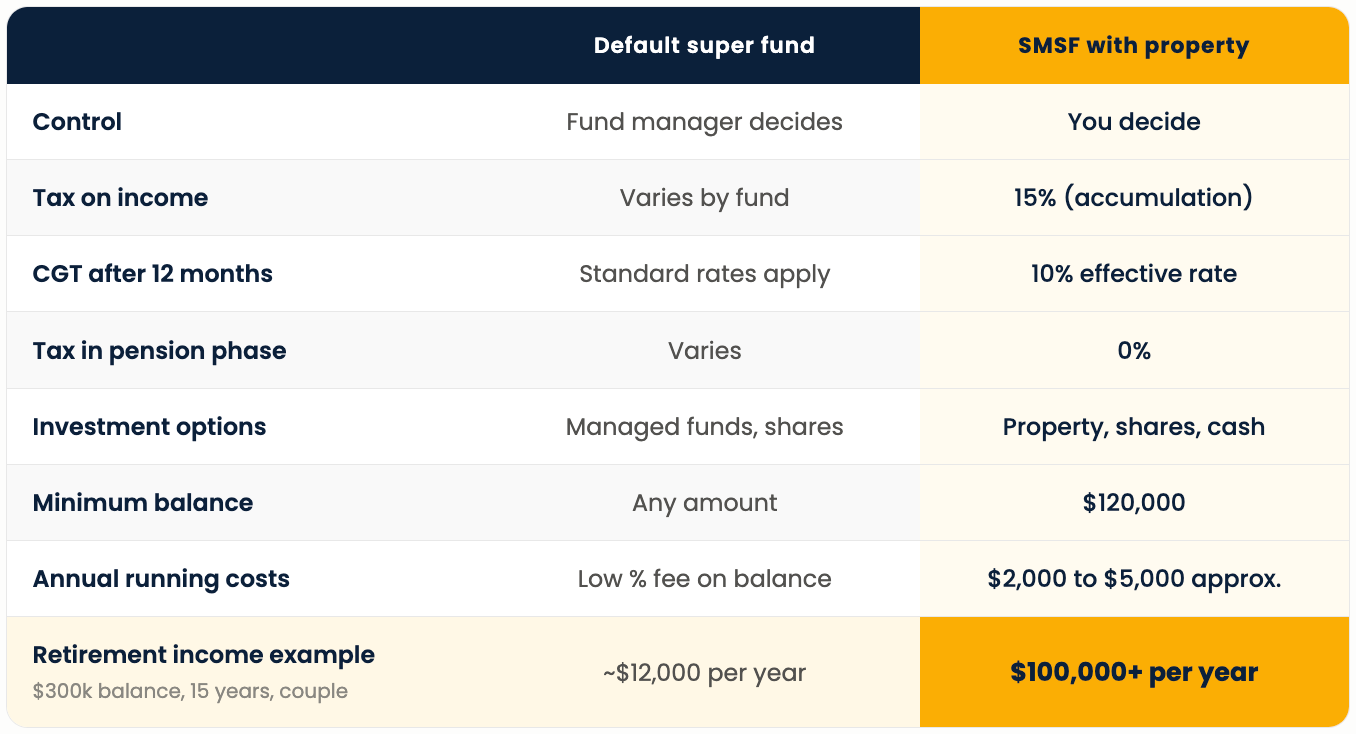

Yes, you can buy property with your super, but only through a Self-Managed Super Fund (SMSF). Rental income is taxed at 15% and capital gains may be completely tax free in pension phase. Following the June 2026 changes, SMSFs can no longer borrow to buy residential property but can still buy using existing fund cash and contributions.

Important Update: SMSF Borrowing Changes June 2026

As of June 2026, the federal government passed legislation ending the ability for SMSFs to borrow money to purchase residential property through a Limited Recourse Borrowing Arrangement (LRBA). This change is prospective, meaning existing LRBAs are fully protected. There is a 45-day transition window for arrangements already in progress.

SMSFs can still purchase residential property using existing fund cash and contributions without borrowing. The tax benefits remain unchanged.

What Is an SMSF?

A Self-Managed Super Fund (SMSF) is a private superannuation fund that you manage yourself, rather than relying on a retail or industry fund to manage on your behalf.

As trustee of your own fund you control where your super is invested, you can invest in assets like property, shares, and cash, and you are responsible for ensuring the fund meets all legal and compliance requirements set by the ATO. SMSFs can have up to six members, which is why many Australians set them up with a partner, family members, or business partners to pool superannuation balances.

How Does Buying Property Through an SMSF Work?

When your SMSF purchases an investment property, the fund owns the property, not you personally. This is an important distinction.

The general process looks like this:

Set up your SMSF by establishing the fund with a trust deed and appointing trustees

Roll over your existing super balance into the SMSF

Ensure the fund has enough cash to cover the full purchase price, stamp duty and costs.

Purchase the investment property with the SMSF settling and becoming the legal owner

Collect rental income which flows back into the SMSF and is taxed at the concessional super rate of 15%

What Is a Limited Recourse Borrowing Arrangement?

An LRBA was the only approved way for an SMSF to borrow money to purchase an asset like an investment property. It was a loan structure specifically designed for super funds.

As of June 2026, SMSFs can no longer use an LRBA to purchase residential property. The information below applies to existing arrangements already in place, which remain fully protected.

Under an LRBA, the lender's recourse is limited to the asset being purchased. If the fund defaults, the lender cannot pursue other SMSF assets. The investment property is held in a bare trust until the loan is fully repaid, at which point full ownership transfers to the SMSF.

Not all lenders offer LRBA loans and lending criteria are generally stricter than standard investment loans.

What Are the Rules Around SMSF Property?

The ATO has strict rules governing what an SMSF can and cannot do with property. Getting this wrong can result in serious penalties.

Key rules include:

Sole purpose test: The property must be acquired and maintained solely to provide retirement benefits for members

No personal use: Members, relatives, or related parties cannot live in or rent the residential property at any time

Related party restrictions: An SMSF generally cannot purchase residential property from a related party

Commercial property exception: SMSFs can purchase business real property from a member at market value and lease it back to the member's business at market rates

Renovation limits: Significant structural improvements cannot be made using borrowed money

No equity access: You cannot use the rise in property value inside an SMSF to borrow for further investments

What Are the Tax Benefits of Buying Property in Super?

This is where the SMSF strategy becomes particularly attractive for long-term property investors:

Rental income is taxed at just 15% inside the SMSF (compared to your personal marginal tax rate, which could be up to 47%).

If the investment property is sold while the SMSF is in the retirement phase, the capital gain can be completely tax-free.

Costs such as interest on loans, council rates, insurance, and repairs are generally deductible against the rental income.

Owners can claim depreciation on building structure and fixtures, reducing taxable income.

What Are the Risks and Considerations?

SMSF property investing is not for everyone. Key considerations include:

Higher upfront costs: Setting up and running an SMSF involves annual accounting, auditing, and legal fees

Minimum balance required: Most financial professionals suggest a minimum of $120,000 before an SMSF becomes cost-effective

Liquidity requirements: The fund needs sufficient cash to cover ongoing expenses, loan repayments, and member obligations

Compliance responsibility: As trustee you are accountable for keeping the fund compliant with ATO regulations each year

No equity extraction: Unlike personal name ownership, you cannot extract equity from an SMSF property to fund another purchase

Illiquid asset: Property cannot be sold quickly if the SMSF needs to pay benefits or meet expenses at short notice

Borrowing now restricted: Following the June 2026 legislative changes, new residential property purchases using borrowed funds inside an SMSF are no longer permitted

Is SMSF Property Investing Right for You?

SMSF property investing works well for people who:

Have a sufficient super balance to make it cost-effective

Are looking to diversify beyond traditional super investments

Want greater control over their retirement wealth strategy

Can purchase property outright using existing fund cash and contributions following the June 2026 borrowing changes

Frequently Asked Questions

Can I still use my SMSF to buy property after the 2026 changes? Yes, using existing fund cash and contributions without borrowing. SMSFs can no longer use an LRBA to purchase residential property following June 2026 legislation. Existing LRBAs already in place are fully protected and unaffected by the change.

How much super do I need before setting up an SMSF to buy property? Most financial professionals suggest a minimum balance of $120,000. Below that threshold, the annual accounting, auditing, and compliance costs can outweigh the tax benefits

What are the tax benefits of buying property inside an SMSF? Rental income is taxed at just 15% inside the fund compared to your personal marginal rate of up to 47%. Capital gains are taxed at 10% if the property is held for more than 12 months. In pension phase, the capital gain on a sale may be completely tax-free.

Can I live in a property purchased by my SMSF? No. The ATO's sole purpose test requires the property to be held solely to provide retirement benefits to fund members. Members, relatives, and related parties cannot live in or rent the property at any time, including short stays or holidays. Breaching this rule can result in serious penalties.

Can I use equity from an SMSF property to buy another property? No. Unlike purchasing in your personal name, you cannot extract equity from a property held inside an SMSF. Each additional acquisition must be funded from available cash already sitting in the fund.

What is the difference between residential and commercial property inside an SMSF? Residential property cannot be purchased from a related party or used by members at any time. Commercial property has different rules and can be purchased from a member at market value and leased back to their business. Speak to an SMSF specialist accountant before making any decision about property type inside your fund.

Ready to Explore Whether an SMSF Property Strategy Is Right for You?

At Search Property, we help Australians cut through the noise and build data-driven investment strategies aligned with long-term wealth goals. Our buyers agents have helped thousands of clients build wealth through property because we focus on fundamentals, not headlines.

Book a FREE investment assessment call with Search Property. We'll discuss your goals and position, and help you build a clear plan to move forward with confidence.

Frequently Asked Questions

Dropdown

No items found.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)

.png)

.png)