With a significant rate cut by one of the big four banks, Australian homeowners are seeing potential changes in mortgage rates. This article dives into the reasons behind the rate cut, the current economic indicators, and what it means for mortgage stress and future interest rates. Learn about the factors influencing these decisions and how they affect you.

One of the big four banks has cut their fixed loan interest rates, which could signal changes in mortgage rates around the corner.

A lot of this is linked with mortgage stress, so in this article, I want to cover the following points:

If you're interested in my thoughts, definitely keep reading.

Australians Falling into Mortgage Stress

Recently, with interest rates rising and staying high for so long, we've had another 800,000 Australians fall into mortgage stress.

Yes, that does sound like a lot, because it actually is.

I want to cover a couple of key stats around what's happening with mortgages and why one of the big four banks is doing the opposite of what's actually happening out there.

We've been told that:

Inflation is high.

The RBA can't cut rates.

Some suggest that interest rates should actually go higher.

So let's dive into it!

Key Statistics

What we have here is the rate of interest rate changes. This shows us the percentage increase from our existing cash rate, and Australia is above Canada, New Zealand, the United Kingdom, and the United States.

When economists in America say that the Fed is likely to cut rates, with an 87% to 90% chance of that happening in September 2024, what does that mean for Australia, where we've increased our rates at a faster pace? It's been steeper, yet we're not talking about interest rate cuts until 2025.

One of the big four banks, CBA, has suggested that they think the first interest rate cut will happen in November 2024.

If you're reading this in August, we're only a few months away from finding out definitely what's happening.

However, what is really putting pressure on all of these banks to not decrease their rates, and the RBA to not increase or decrease rates? We're in a very tricky situation.

I'm going to make it really simple for you:

If the RBA were to increase rates, they would also have to look at:

Unemployment

Retail spending

Right now, these two figures are looking very dire. So if you looked at these two numbers, you'd say: well, we need the RBA to cut.

Whereas, if you look at inflation, you'd say: the RBA needs to increase rates, and hence why we have a stalemate.

This is why the RBA isn't moving the interest rate; they're just hoping for a soft landing at this point.

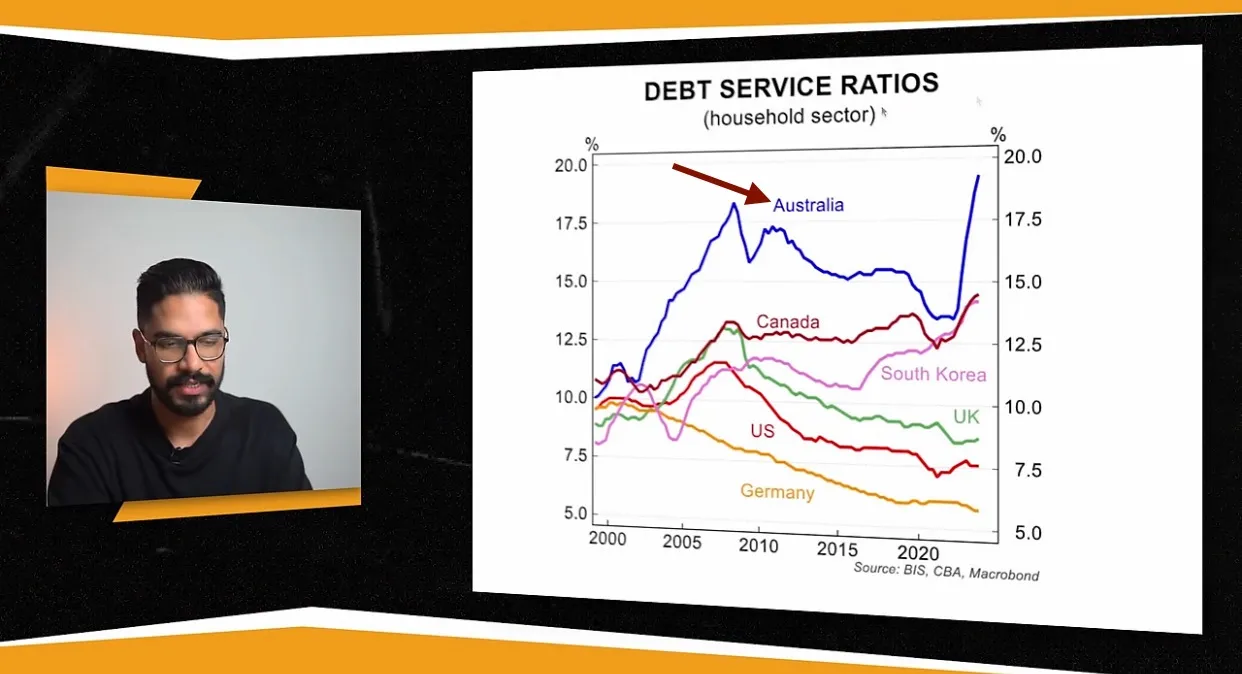

This graph here is pretty telling. It's the debt service ratio for the household sector. It's effectively the percentage of how much you put towards servicing your debt.

What we can see is since 2020, we've just been in a vertical line up, and that's because times are really tough here as interest rates have increased and people borrowed at such low figures. Now we're having to repay the same debt at almost two to three times more in terms of interest expense, which is pretty crazy.

Here's something from Roy Morgan research. What we can see is the percentage of mortgage stress for owner-occupied mortgage holders.

Since 2020, with all those lower interest rates, we've continued to see it rise.

However, what's interesting is that we're starting to plateau and potentially start dropping off.

There are a couple of reasons for this, but most notably, people have found a lot more equity in their properties, so they have a couple of choices.

If you decide to sell, the percentage of people in profit right now is at almost all-time highs, which means that if someone did buy two years ago and then decided they couldn't hold this property any longer and wanted to sell, they would probably walk away with more money in their pocket.

The worst-case scenario would be that if interest rates went up, people would be forced to sell, but the market pulled back. If this happened, you would be forced to sell at a loss, which would mean more people would hold on to those properties, leading to an absolute collapse.

One thing that could further emphasise the big problem when it comes to mortgage stress, and it could get a lot worse, is employment.

Take a look at this graph:

The blue line represents applications per job ad.

The red line represents the job ads themselves.

What this effectively says is:

This will start causing the unemployment number to rise, putting further pressure on the RBA to decrease rates.

Now, after knowing all this, you may ask yourself: why would one of the big four banks come out and start cutting rates?

Let's dive into which bank it is and why they're actually doing this.

The speculation is still out there. As I mentioned, because inflation is so high, people think that interest rates will continue to go higher. But I'm going to tell you a little bit more in a second about why this is so important and why you should pay attention.

The report also added:

If you think back a couple of years ago, where variable rates may have been at 3.5% to 4%, whereas fixed rates were much lower than that, that's when we had rates below 2%.

I know it sounds crazy at this point, but they were at 2%.

What a lot of people did was they started fixing their rates at that point because the fixed rates were lower than the variable.

Now, let's work out:

Why banks look at fixed rates and variable rates

Why it could be a strategic move

When a bank says, "I'm going to increase the fixed rate above the variable rate," you might think: "Well, I can pay the variable rate and have maximum flexibility, so why would I lock myself in for the next 3 years at a higher rate? I'll just take the variable rate."

To understand why the bank thinks like this and what their strategy is, they believe that:

If they offer a 3-year fixed rate and say: "Okay, we're happy to give you 6%," you may think: "That's a no-brainer because I'm already paying 6.5% on variable. Sure, I have flexibility, but what if interest rates go up like they have been?"

You go ahead and fix the rate at 6%.

Although the variable rate right now is at 6.5%, why would the bank do this?

In their opinion, they believe that the interest rate in 3 years will actually be much lower than 6%.

However, because you locked yourself in, they're going to start making profits on the difference.

Let's fast forward 24 months from now, and you find that the variable rate is 4.5%, whereas you fixed your rate 2 years ago at 6%. This gap is the price you pay for certainty, and this is where the bank profits.

It does work the other way around, where they believed interest rates were going to be lower, and they ended up with a fixed rate that was much lower due to volatility, allowing many to profit.

If you had fixed your rates at 2% and the variable rate over the next 3, 4, 5 years turned out to be 4.5% or 5%, that gap is your profit. So it does work both ways.

However, in most situations, emotions get the better of us, and many people fall for the trap, thinking: "Interest rates have been so high for so long, I think they're going to go much higher."

As a result, they’ll fix their rates at what looks like a lower rate in the short term but over the long term, it could actually work out worse for them.

I know this really well because I did the same thing with my first property. I looked at the interest rates, saw the fixed rates and thought, "Yeah, this makes sense."

As soon as the fixed rates started dropping, I fixed my rates, and over the next couple of years, I saw the variable rate go lower and lower. My mood dropped, knowing I was losing money because I made a silly decision.

It will be very interesting to see over the next couple of months who makes a move first. Right now, NAB made it on one product, but they could easily change their minds next month and increase the rates again.

However, I don't think this is a notable move yet.

If we start seeing three to five banks do this across different products, that will be a telltale sign that they believe, and they have people much smarter than you and I (although that is arguable), we could find ourselves getting a hint or an insight into what they believe the interest rates will be in the next 24 to 36 months.

Right now, we probably are closing in on the end of this rate-hiking cycle. If you look at inflation alone, you might believe there are one or two more rate hikes to come, and you should budget for that.

However, if you look at the economy as a whole, it's hard to believe they will increase interest rates further. If they did, I think the steep fall afterward would be even more significant.

I hope you’ve learned a lot from this article.

I'll catch you guys in the next one.

Thanks, guys!

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)

.png)

.png)

.png)

.png)