Australia's job market is facing significant challenges, with concerns over wage growth and economic stability. Discover key insights and data on how rising prices and employment trends are shaping the future of the Australian economy. Dive into expert analysis and predictions to understand the broader implications for personal finance and real estate investments.

However, we have some serious concerns when it comes to the:

Job market;

Wage growth; and

Everything in between for the Australian economy.

In this article, I want to figure out:

If you're interested in what my thoughts are, definitely keep reading.

Rising Australian Prices and Economic Concerns

Now, I occasionally talk about the Australian economy, and in this article, we're going to go through some data as well as some of my thoughts on why it seems like you could go and talk to five people over the weekend and find different opinions.

Some will go: Oh, my rents are going up.

While others are saying: My rents are actually okay.

Others with a mortgage, have their rates going up, while others have a house that they are using equity from to buy another house.

It's actually crazy to think how divided the country has become when it comes to personal finance.

So let's go through some key figures and then we're going to wrap it all up together and figure out what happens next because: Hey, who doesn't love crystal ball predictions because we always get them right, don't we?

I clearly don't, so let's just continue.

Current State of the Job Market in Australia

Yara Capital Chief Economist Tim Tui warned that Australia is not creating enough jobs to soak up the large numbers of Migrant workers arriving, which risks pushing the unemployment rate sharply higher.

This means we have way too many people relative to how many jobs are being created.

The latest figures that came out of Seek also suggest the same thing.

So what we have here are the June 2024 numbers, and what we can see:

National job ads month-on-month have reduced by 1.5%.

National job ads 2024 June versus June 2023 are down 17.1%; and

Applications per job ad month-on-month have increased by 3%.

Now, this graph here showcases exactly what's been playing out.

In the red, we have job ads. In the blue, we have applications per job ad.

During the period of the lockdowns, job ads went down, but applications per job went up.

Why? Because if you think about it, people were stuck at home, probably lost their job, so they’re going: Now, I need to go find a new job.

Whereas, most businesses were shutting down and locking down, so they were like: We can't actually advertise for as many roles.

Now what we're seeing is the inverse effect and what we've experienced in the last couple of years is that the number of applications per job ad has reduced, whereas job ads increased.

Why? Because as the lockdowns got lifted, some companies took off and needed more people to work there.

We, as individuals, also got a lot of stimulus from the government (what’s up, government), and they expected us to use that money in restaurants and cafes. Given that we weren’t travelling, everyone’s like: Hell yeah, I’m going to spend all that money.

This meant that cafes, restaurants, companies out there, and services like ours—the buyer’s agency, also took off, so we needed to hire more people.

However, what we saw during that time was it was very hard to find the right talent, because there were:

Now what we’re seeing is the opposite trend starting to play out again.

Job ads from companies are starting to reduce; but

The number of people applying for these jobs has started to increase.

My theory behind this is that we have some sectors really suffering during a period like this.

We've seen so many companies go bust, especially in the building and construction industry, and that's largely because of interest rates.

Now, if you think about this with interest rates:

Let's cover this off from a business perspective.

If you have interest rates higher for longer (which they actually have been), you may have those companies carrying some potential debt against things like inventory. They might be a coffee machine, there might be machinery, and there might just be business loans just to get the business up and running.

If the interest rates have stayed higher for longer, the repayments on those loans stay higher for longer, which means it's starting to squeeze.

What would further compound this problem is when customers aren't spending as much.

Now again, if you've got interest rates also high, you then have people suffering from higher rentals, because there's not enough properties being built and that's because no one wants to take on another loan.

If you actually think about this, for you to go out and build a new home, not only would you have to continue renting your place, or if you're living in a place that you've already got a mortgage on, you would still have to do this, plus you would have to take up a loan for the build and the land component.

Now, the construction loan would be done in stages, but effectively, it’s like 12 months at minimum to build a house.

So for 12 months, you’ve got to effectively pay two mortgages or rent, plus another mortgage, and not everyone can do that, especially right now, when the cost of living crisis is where it’s at.

As a result, you've got people who aren't willing to spend as much. If they're not willing to spend as much at these stores, cafes, and restaurants, you suddenly have these companies not having to hire as many people, and the negative loop flow continues.

This is why we're in a position now where if we're starting to see these numbers invert where job ads are going down and there are more people applying for work, you are going to start seeing the unemployment number go up.

Now, what's very important to bring this all back home is the Reserve Bank of Australia (RBA) has come out previously, and although they have had a track record of lying to us about whether interest rates will go up or down, they have said one thing which is: If unemployment starts going up, and it hits 4% or 4.5%, we will have to cut, and this is irrespective of what inflation is doing.

Whether you're going to make a decision on continuing to rent or whether you're going to buy your own property, take out more debt, it is important that you know it is not just about inflation. You have to consider the economy's health in general as well.

This graph here is the unemployment rate versus job ads. What you can see is that job ads usually will be the first indicator that goes up or down, and then the unemployment rate follows.

If you go back in time and look at 2012, the blue, which is the job ads, is inverted. It’s the opposite. So if the number goes higher, it’s actually going lower—in this case: the unemployment rate. This is just to show you the correlation between the two.

As you can see, job ads are actually going down although in this graph it's inverted, so it’s going up.

Now, you’ll see that this goes first and then unemployment goes up.

You can see it in the 2020 section, where you’ve suddenly seen the blue line go up first, then the red one follows.

Now what we're seeing is the blue line is so much further ahead.

The correlation between the two is very closely linked. So if we're starting to see this gap, either one of two things will happen:

You’ll see job ads actually go up during this time; or

You're going to see the unemployment number go up.

Either way, you're going to see some sort of volatile change coming soon in the next six months, and that's why you need to stay prepared.

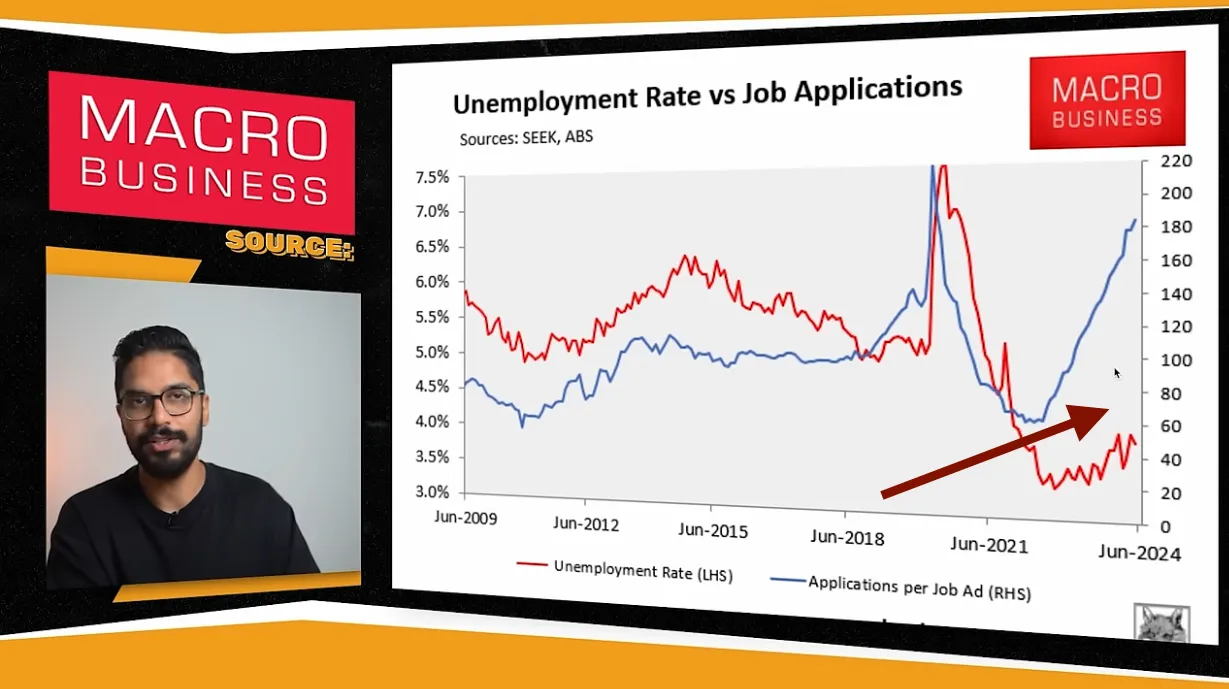

To further emphasise this point and bring it all home, let’s look at the unemployment rate versus job applications.

You can see that this graph has never had such a big gap between the two lines: one being applications per job ad, and the other being the unemployment rate.

This means that a lot of people are applying for jobs, and there’s just not enough out there.

Now, what doesn’t help this situation is where consumer sentiment actually is.

Consumer sentiment is effectively just a gauge of how negative or positive people are feeling out there.

Are they optimistic that the market’s great? (I’m going to put my money into the markets and I’ll make some more money); or

Are they negative about it, suggesting that we may see some sort of crash and therefore they’re going to hold back their money?

What you can see here from Westpac Economics is the number of 100 being the average. So that's the balanced market.

Anything below this number is fearful. Anything above this number is greedy.

So if you think about Warren Buffett's advice to buy when others are fearful and sell when others are greedy, this would be a really good indicator.

Now, what you can see is that we’ve got consumer sentiment at these lows for the longest period of time since 2008. As this graph covers off, it’s at points that we’ve only experienced twice before in the last 20-odd years, and this was during the global financial crisis (GFC) and then we had the lockdowns.

So what you can see is that during the GFC, it seemed like we were there for a little bit, and then we bounced up.

During the time of the lockdowns, we were there for a brief couple of moments, and again that double dip was because we ended up having lockdowns again, and then we shot up.

However, now, although the consumer sentiment is slowly rising, we’re still getting affected by the fact that inflation is higher than normal. This means interest rates could go up in the next meeting, and that is holding a lot of people back from actually going out and purchasing investment properties.

Final Thoughts

If I’m to conclude all of this and bring to you what my thoughts are around real estate investing, and why it still could be a really good opportunity for you, it’s because you want to be buying when there’s fear out there.

You also don’t want to buy when you’re about to lose your job, and this is why it is such a complex conversation.

Is it just interest rates going up and down? No. Because there’s cause and effect of that.

If you then marry that up with building approvals and where we are at such shockingly low numbers when it comes to the supply of new quality homes, you’re then going to realise:

YET….

Why?

Well, it comes down to one simple thing: supply and demand.

I know I’ve covered a lot of data points here and shown you some graphs.

So here’s the key takeaway from the entire discussion: Even though the Australian economy could be sick, or it could go through a recession, or there’s a lockdown, that does not automatically mean that property prices will go down or up during that period.

If you look at 2008 and 2009, we had the global financial crisis (GFC), we had a small blip in terms of prices, and they bounced straight up.

If you look at something like 2016 to 2018, you’d be like: the economy was actually doing pretty well.

However, you had property prices go down, and that’s because the availability of credit was the main factor there.

Then you look at the lockdowns. During these times, the Australian economy went through a recession. However, interest rates went down, and you also had unemployment go up, but property prices went on the biggest run ever.

So there’s a lot to unpack, especially when it comes to economics and looking at the housing market.

That’s why so many people get stuck at one, two, or three properties if they’re lucky, while some will never even make that purchase.

I have conversations like this every day, whether it's:

Strategy sessions;

Discovery calls; or

Talking to the client account managers who are talking to people every day, suggesting that some people just have analysis paralysis.

For me, personally, these numbers are important but they're not everything.

What you want to do is go and build a property portfolio with a strategy, and have the emergency funding in place.

If you go and stretch yourself during a time like this, it might not be the smartest decision, especially if you’re in a job that is in a volatile job market.

If you're someone who’s confident, runs your own business, and can forecast the next 24 months, and things are looking good, I would definitely be more aggressive now, especially because:

We have a severe supply shortage; and

There’s so much negativity out there. We are so far from the top.

Generally, what makes up a top in the market when you’re about to see a collapse is when everyone is euphoric. Everyone thinks the market can never come down, and trust me, it doesn’t feel like that right now.

I hope you guys have learned a lot from this article.

I'll catch you guys in the next one.

Thanks, guys.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.webp)

.png)

.png)

.png)