How Much Deposit Do I Need to Buy a House in Australia?

Is buying a house in Australia with a small deposit possible? Despite common beliefs, entering the property market now is more possible than you might think. I'll break down the upfront costs, including stamp duty, conveyancing, and inspections, and show you how even a modest deposit can kickstart your property investment journey. Keep reading to learn how you can achieve your homeownership goals with smart financial strategies.Is buying a house in Australia with a small deposit possible? Despite common beliefs, entering the property market now is more possible than you might think. I'll break down the upfront costs, including stamp duty, conveyancing, and inspections, and show you how even a modest deposit can kickstart your property investment journey. Keep reading to learn how you can achieve your homeownership goals with smart financial strategies.

If you’ve been hearing that buying a house in Australia is impossible right now, here’s the truth: it might be more achievable than you think. Even with a small deposit, you can start your property journey with the right numbers, knowledge, and strategy.

Let’s break down how feasible it really is to buy your first property, what upfront costs to expect, and how a simple mindset shift can get you into the market faster.

How Feasible Is It to Buy with a Small Deposit?

When it comes to investing, you often hear price points between $450,000 and $700,000, with most examples sitting around $450,000 to $550,000.

You might wonder: “Where can I buy a house for $500,000?”

The truth is, there are still opportunities out there, just not always in your backyard. Whether you’re based in a metro area or the east or west coast, many investors don’t realise what’s available a few hours away.

So, let’s dive into the real numbers.

Real Numbers Speak Louder Than Words

Say you’re buying a property for $500,000. You have two options for your deposit:

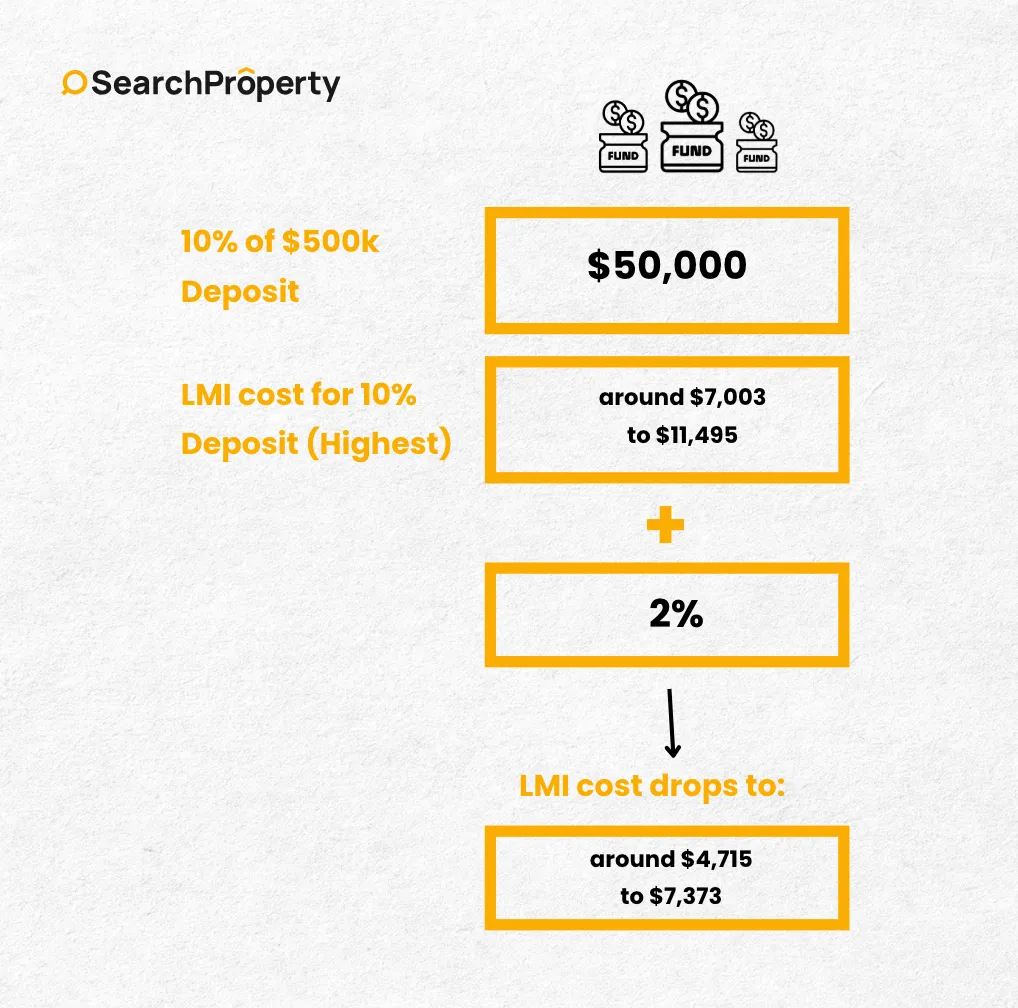

10% deposit: $50,000

12% deposit: $60,000

Now, you might ask, “Why would I put down 12% when I can do 10%?”

If you go with 10%, your LMI might cost around $7,003 to $11,495. However, by putting in an extra 2%, your LMI can drop to around $4,715 to $7,373. It’s not mandatory to go higher, but this simple adjustment could save you thousands upfront.

Why the Right Mortgage Broker Matters

It is possible to purchase a property with less than 20% deposit, but not every mortgage broker knows how to structure this properly.

Too many Australians are told, “You can’t buy with less than 20%.” That’s not true, and believing it often stops people from ever getting started.

Having the right mortgage broker can be the difference between sitting on the sidelines and taking action now.

Other Upfront Costs to Expect

When you’re buying property, your deposit isn’t the only cost. You’ll also need to budget for stamp duty, conveyancing, inspections, and potentially a buyer’s agent fee.

Stamp Duty - For a $450,000 property in Queensland, stamp duty would be around $7,000.

Conveyancing - Your conveyancer reviews and manages the contract to make sure you’re protected legally. They ensure all terms are met and changes are communicated clearly so you don’t end up in a bad deal.

Pest and Building Inspection - A pest and building inspection can cost anywhere from $400 to $2,000, depending on your location. Always include this condition in your contract. It protects you from buying a property with hidden damage, the kind that could cost you tens of thousands later.

If a deal looks too good to be true, it probably is. Always do your due diligence before signing anything.

Understanding the Role of a Buyer's Agent

Some buyers rely on the selling agent and assume it’s “free help.” It is key to remember: real estate agents work for the seller, not you. Their goal is to get the highest possible price.

A buyer’s agent, on the other hand, represents you. They negotiate on your behalf, help you find the right property, and ensure you don’t overpay.

Our buyer’s agent service is a fixed fee, not commission-based. That means we’re motivated to get you the best value and results, not the highest sale price.

Shifting from a Saving Mindset to a Growth Mindset

If your goal is financial freedom, you can’t just focus on saving more; you need to focus on earning and leveraging more.

Saving alone is limited. You can only save what you earn. When you use your money strategically by investing earlier and leveraging good debt, your earning potential becomes unlimited.

The key is not to wait for the perfect time. It’s about starting with what you have and building from there.

Why Time in the Market Matters

When it comes to building wealth through property, time in the market beats timing the market.

Buying with a smaller deposit allows you to control more assets earlier, giving your properties more time to grow in value.

Instead of saving for years and missing out on growth, you can start sooner and use that time to your advantage.

Ready to Get Started?

Buying a home or investment property in Australia doesn’t have to feel out of reach. With the right strategy, a clear plan, and a trusted team by your side, you can start building your property portfolio sooner than you think.

If you’re ready to explore your options, book a free discovery call with our team today. We’ll walk you through what’s possible based on your goals, deposit, and budget so you can take your first step toward financial freedom with confidence.

Disclaimer: Important Notice for Readers

By reading the content provided on this blog, you acknowledge and agree to the terms outlined in this disclaimer, binding yourself to its provisions unconditionally.

This blog presents information for informational, educational, and general non-advisory purposes only. It's important for you, the reader, to understand that the information provided does not take into account your specific personal, financial, or other circumstances. Consequently, we do not offer legal, financial, investment, or taxation advice, recommendations, or guidance. Before acting upon any information from this blog, you are strongly advised to consult with an independent professional, including legal, financial, taxation, accounting, or other relevant advisors, to verify the information’s relevance to your particular situation.

The information is provided in good faith, derived from sources believed to be reliable. However, we do not guarantee the accuracy, completeness, or applicability of the information to your individual circumstances, needs, objectives, or financial situation. The information may be selective and has not been independently verified. Therefore, it should not be the sole basis for any decision-making.

We expressly disclaim any liability for errors, omissions, or inaccuracies in the information, as well as any direct or indirect losses, damages, or expenses that arise from relying on our content, regardless of the cause, including negligence or other factors. Your engagement with this blog is entirely at your own risk.

Please be aware, we do not hold an Australian Financial Services Licence as defined by section 9 of the Corporations Act 2001 (Cth), nor are we authorised to provide financial services, and we have not provided financial services to you.

Disclaimer: Search Property Pty Ltd (SP) does not provide financial or investment advice and does not hold a financial services license as defined in the Corporations Act 2001 (Cth). Any advice given by SP is general in nature and does not take into account your personal circumstances or objectives, financial situation or needs.

.png)

.png)

.png)